Save over 60%: The Magic of Tuition and CTC Tax Credits

Evelyn Jacks

Did you know that you can reduce the cost of your tuition fees by over 60% (depending on your province of residence, thanks to the refundable Canada Training Credit (CTC) and the non-refundable Tuition Fee Amount? This can substantially reduce your tuition fees payable, in particular here at Knowledge Bureau. Here’s how it works?

Understanding the Tuition Fee Credit. Most people know that the tax system allows for a non-refundable tax credit on the T1 known as the Tuition Fee Amount. But, you need to have taxes payable for it to work to your advantage. If you don’t, the claim may be transferred from the student to the supporting individual; that is, a parent, a spouse or a grandparent.

But there is a maximum limit to this transfer and it is not indexed: only $5000 can be transferred and unfortunately this amount is not indexed to inflation. It’s a tax reform change that is long overdue as the cost of education has increased substantially over the years.

Another option: if there is no supporting individual, or the student would prefer to save the amount to reduce taxes when earning income later, the unused tuition amounts may be carried forward to future years. The claim must be supported by keeping form T2202 Tuition and Enrolment Certificate – keep it on hand in case CRA wants to see it. Knowledge Bureau students can login and access this in their VIP Graduate Lounge.

New Educational Institute Criteria. Generally speaking the tuition fee credit is claimable when post-secondary education is taken at a qualifying post-secondary institution. For tuition fees paid after 2016 to acquire occupational skills courses taken at a university, college or other post-secondary educational institution (such as Knowledge Bureau) fees paid will be eligible for the Tuition Tax Credit. This is true even if the courses are not at a post-secondary level, so long as the student is over 16 at the end of the tax year.

Adjusting Prior Filed Returns. The claim for tuition fee amounts has also been impacted by a series of changes over the years so that if you need to adjust prior filed returns to recover a missed claim or correct an error or omission, which you can do from Tax Year 2016 forward in 2026. This includes adjustments for some now-eliminated tax credits the federal return and provincial calculations as well.

The Federal Education & Textbook Amount was eliminated in 2017, leaving only the Tuition Fee Credit on the Federal T1. However, several provinces have retained the Education Amount. This includes Manitoba, Northwest Territories, Nova Scotia, Newfoundland and Labrador, Quebec and PEI. The provinces of ON, BC, AB have eliminated theirs.

Provincial Tax Credits. Notably, Saskatchewan offers the Graduate Retention Program (GRP), which provides a non-refundable tax credit of up to $24,000 for post-secondary graduates who live and file income tax in the province and Alberta has a training tax credit associated with apprenticeships.

Claiming the Canada Training Credit. The Federal Budget of 2019 introduced the Canada Training Credit (CTC), which is a “notional” amount that accumulates to a lifetime maximum of $5000 when the personal tax return is filed.

It’s a refundable tax credit and it reduces tuition fee amounts otherwise claimable, that’s based on income earned in the prior tax year and your age. A 2019 tax return had to be filed to get the first annual credit of $250 in 2020, so if that filing was missed, it’s important to catch up.

The age range to qualify is 26 to 65.

Income Criteria. In order to claim this refundable tax credit, the taxpayer has to have claimed eligible tuition fees for the year and have both a minimum working income and meet a maximum net income threshold in the prior year. Here is the qualifying criteria in chart form:

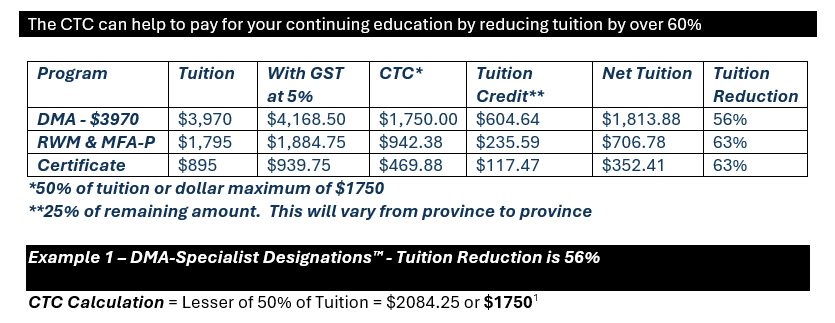

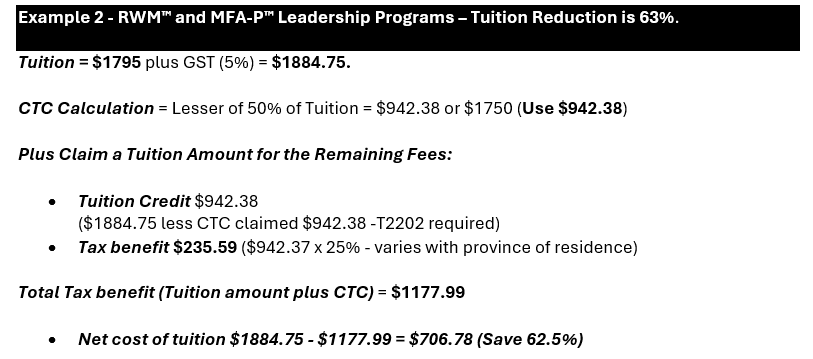

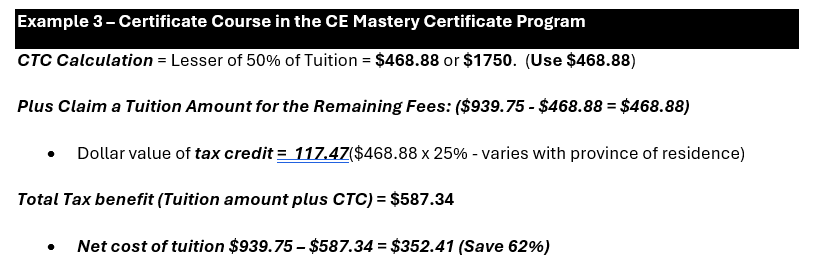

How it works. Here are a few examples of how this applies to the Spring Session tuition fees for certificate, diploma and designation programs at Knowledge Bureau:

Plus Claim a Tuition Amount for the Remaining Fees:

[1](Note: - if no taxes payable, this $1750 CTC is fully refundable when you file your tax return

- Tuition Credit = $2418.50 ($4168.50 less CTC claimed $1750 -T2202 required). Dollar value of tax credit = $604.64 ($2418.50 x 25% - varies with province of residence)

Total Tax benefit (Tuition amount plus CTC) = $2354.64

- Net cost of tuition $4189.50 - $2355 = $1813.88 or $302 per course (save 56%)

Bottom Line: The combination of the CTC and Tuition Fee Credit is lucrative. Be sure to use them to reduce your training costs and adjust prior filed returns if you missed this.