Record Number of Tax Returns Filed in 2026

It looks like tax season 2026 could be the biggest one we’ve seen in the history of filing in Canada, proving once more that Canadians are extremely tax compliant and that filing a personal tax return is the most important triggers for long term wealth planning in this country. But there is a shortage of qualified people and now is the time to do something about that before tax season 2027.

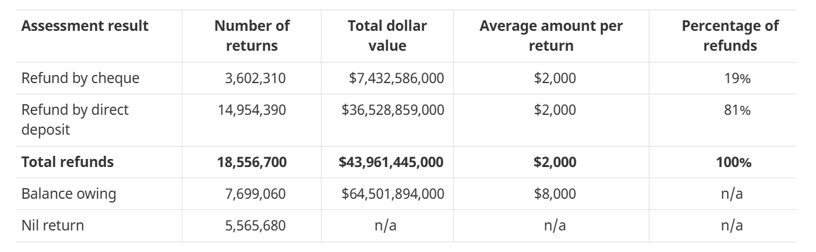

The Tax Filing Numbers Tell the Story. This tax filing season, February 6 to July 6, over 32 million tax returns were filed. It’s interesting that the government, for some time now, no longer does the exact math for the exact amount of refunds or balances due.

So, we did it. The average refund was $2,369 representing close to $200 a month in overpaid taxes – an interest free loan to the government. The vast majority - 81% - of those with refunds chose to receive them electronically.

Even more eye-popping was the balance owing by the 7.7 million taxfilers: $8,378. That’s just under $700 a month that needed to be saved to be ready for the tax filing deadline.

There were 5.6 million tax filers who had a nil income return. These folks are the targets for automatic and deemed tax filing coming soon from the federal government. But it would be wrong to think these are “simple” tax filing profiles. There can be lots of reasons for a nil return, including net income reductions with capital cost allowance claims or income averaging provisions available to farmers and fishers, capital gains offset by losses, or significant use of other available and legitimate tax preferences.

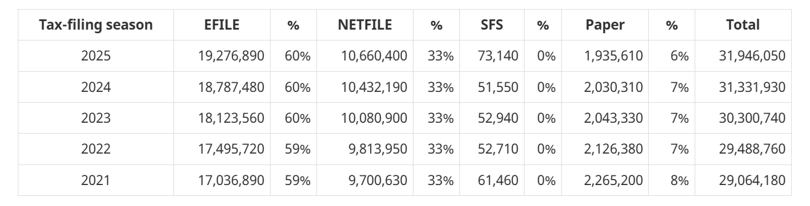

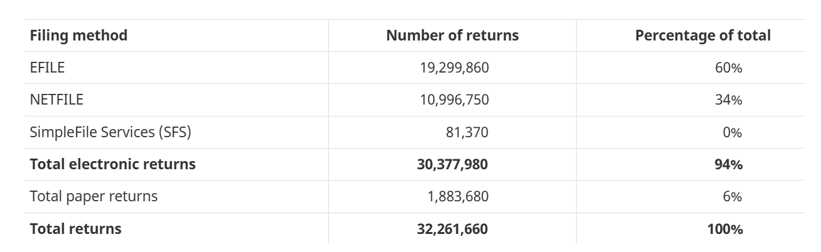

EFILERs Rule. The preferred way to file a tax return by far was with professional EFILERs, a trend that has continued over the past couple of years.

This follows recent trends for initial annual assessments. It’s interesting to note that SimpleFile Services had a bit of a pickup this year; but still insignificant, which poses a challenge for the automatic tax filing initiative: